You know what I mean. Are you keeping regular now? I want to take a minute and talk about our current regulatory environment. Hear me out before you roll your eyes and click out, especially you Realtors. Lenders know exactly where I'm going, but the real estate community, not so much. Now, before we talk about regulations and compliance, let me be clear. We need regulators and we need compliance. It is very important and sorely needed in the industry. Okay, got it? Good. I'm not saying CFPB sucks with our ideas or stupid or compliance is not needed. They are important and needed. However, that being said, what we're doing right now in this industry, the regulations or over-regulations, that's not working. And it can be seen in just about every nook and cranny in our industry. Let's hit this from a hundred thousand-foot level first. Easy point to be made here. If it was working so well, we wouldn't have politicians vowing to overhaul and repeal it. Hashtag Dodd-Frank. Our current regulatory environment is so troubling, it's actually on our politicians' radar. Nuff said. We can move on. Now, from a 10,000-foot level, as you all know, Wells Fargo announced they would be raising their minimum credit score for FHA loans. What does it have to do with regulations, Ryan? Plus, my lender of choice isn't Wells Fargo. Well, one, just because your lender of choice is lender X down the street doesn't mean this won't affect him or her, and you and your clients, for that matter. The average mortgage lender on the street sells their mortgages to places like Wells Fargo, so when they change their guidelines, so do the lenders on the street. So, it will affect you too. Wells did this because their mission...

Award-winning PDF software

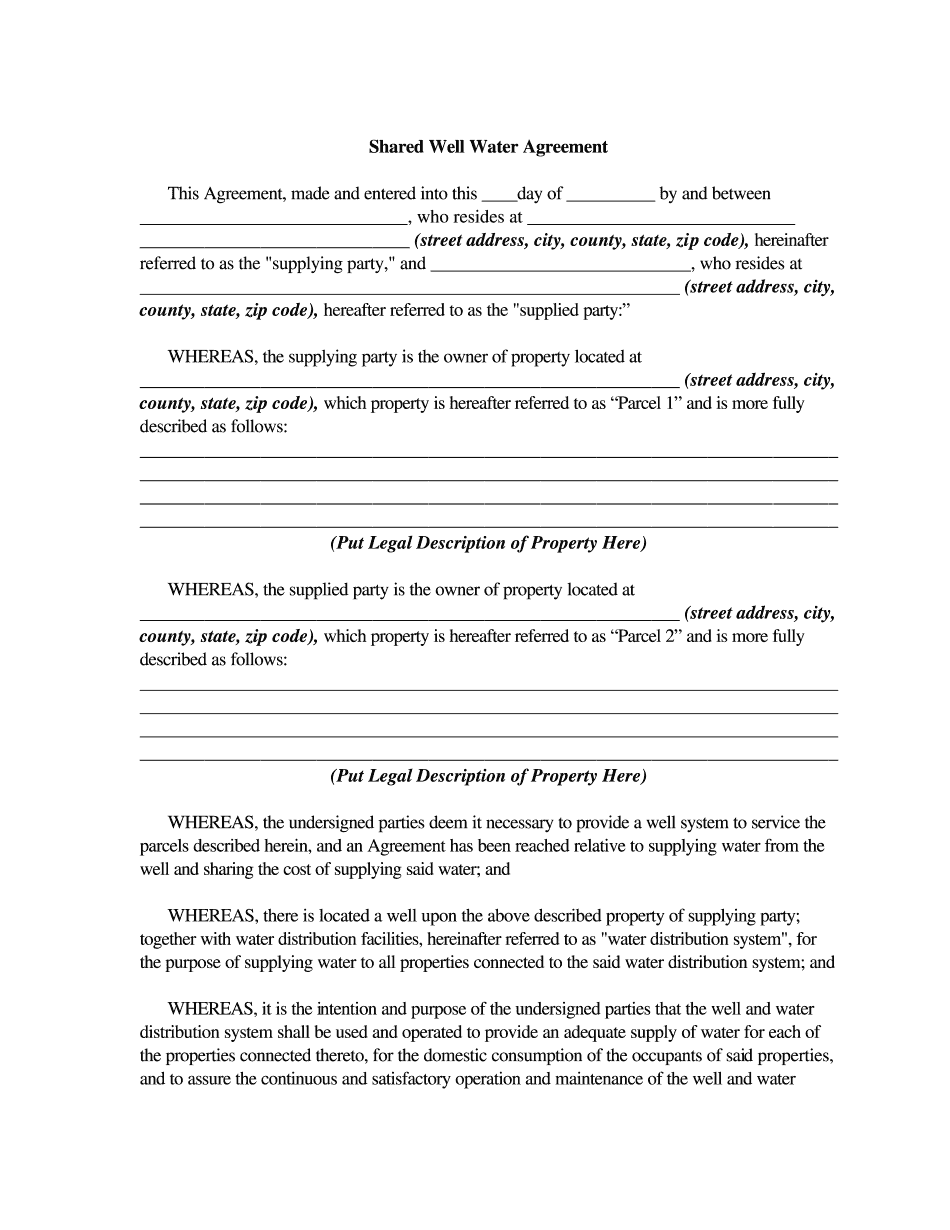

Fha Shared Well Agreement Requirements Form: What You Should Know

Download Now! FHA guidelines and minimum standards for properties served by a shared well (Page 1-21d) — HUD Archives The minimum FHA Loan Standards for properties serviced by wells are: ● The Mortgagee must confirm that the Shared Well has a Shared Water Agreement — Fill Online, Printable, Fillable, Blank Fill The Shared Water Agreement, Edit online. Sign, fax and printable from PC, iPad, tablet or mobile with filler Instantly. Try Now! FHA guidelines and minimum standards for properties serviced by wells (Page 1-21e) — HUD Archives This form is intended to be a starting point and should be reviewed and modified by an attorney prior to being finalized. Each state has different legal rules Maximum number of shared wells allowed? — HUD Archives There is no limit to the number of wells a house can be serviced by the same shared well provider. Share Wells and Water Services : An Example of A Shared Well Agreement — HUD Archives Shared well owners and their representatives must be aware of the important benefits and conditions that may be included in the Shared Well Water and Wells Agreement (WWA). The agreement should address: A mutual understanding and acceptance of a common contract, both parties acting in good faith and without duress. A right to require that Shared Well Water and Wells contractors be at least 18 years old. A right to a written appraisal of services for water and Well installation. No charge in excess of 50 of property improvement costs will be charged to a water or water service contractor in any year that there has been a breach of the conditions of the agreement. An example of a shared well agreement would be: Form 2025 Shared Well Agreement Conditions — Fill Online The Water and Well agreement should be clearly written and signed by the two parties and its contents should be kept for four years. The agreement should also state the following facts, which in accordance with all current federal and state laws should be provided in writing to the homeowner: A water and well contractor will never provide water to a house under the homeowner's name. No payment can be made for water service after water service has been connected to the home. There must be evidence of water service in the house from any source.

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Well Agreement form, steer clear of blunders along with furnish it in a timely manner:

How to complete any Well Agreement form online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Well Agreement form by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Well Agreement form from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Fha Shared Well Agreement Requirements